Commercial Arithmetic 2 Questions

1. The table below shows the rate at which income tax is charged for all taxable income.

INCOME RATE IN EXCH TWENTY SHILLINGS

On the first shs.116 160 10%

On the next shs.109 440 15%

On the next shs.109 440 20%

On the next shs.109 440 25%

On all income over shs.444 480 30%

Mr. Nyongesa earns a basic salary of sh.54, 450 per month. He is housed by the company and therefore 15% of his monthly salary is added to the basic salary as a taxable income. He is also given taxable medical and transport allowances of shs.4,000 and shs.2,000 per month respectively. He is entitled to a family relief of sh.1, 100 per month.

(a) Calculate Nyongesa’s annual taxable income (3 mks)

(b) Calculate his monthly P.A.Y.E after the relief (5 mks)

(c) If 20% of his basic salary goes towards deductions, determine his monthly income. (2 mks)

2. All employees of silver springs enterprises pay income tax at the rate shown in the table below.

Taxable income (p.a) | Rate sh. Per K₤ |

1 – 3780 3781-7560 7561-11,340 11,341-OVER | 2 3 4 5 |

Mr. Mooka earns a basic salary of sh.12,150 and a house allowance of sh.2800 per month. He is

entitled to a family relief of sh.450 per month. A part from income tax the following deductions are also made from his monthly pay.

- Servicing loan payment sh.450

- Hospital fund sh.260

- Sacco contribution sh.120

Determine Mr. Mooka’s net monthly income. (10 marks)

3. The taxation rates for income earned in a certain year were as follows:

Income Tax Rate

K£ p.a Kshs. Per £

1 – 4512 2

4513 – 9024 3

9025 – 13536 4

13537 – 18048 5

18049 – 22560 6

Over 22560 6.5

After a personal relief of Kshs.1056 per month, Otieno paid tax amounting to Kshs.18,152 that year.

a) How much tax would he have paid if he did not have the personal relief (2 mks)

b) Find his taxable income in K£ that year (5 mks)

c) If Otieno receives allowances amounting to 18% of the taxable income. Calculate his monthly basic salary in Kshs. (3 mks)

4. Chepkemoi bought a new washing machine for Kshs.420,000. Its value depreciated over

the next 5years at the following rates; 15%, 13%, 12%, 9% and 7%. For the next 6 years,

the rate of depreciation remained constant at 5% then the rate of depreciation remained at 4%

each. How long did it take for the value of the washing machine to be 1/3 of its original value?

5. The table below shows income tax rates for the year 2006

Taxable income in shs. Pa | Rate of tax in % |

1 – 120,000 | 10 |

120,001 – 240,000 | 15 |

240,001 – 360,000 | 25 |

360,001 – 480,000 | 35 |

Over 480,000 | 50 |

Nafula is married and claims a tax relief of shs.1,120 per month. She stays in a company house

For which she pays a nominal rent of shs.1200 per month. She found that in a particular month,

her employer deducted shs.4830 as tax. If she is entitled to a maximum insurance policy; relief

of shs.600 per month. Calculate her monthly salary. (10mks)

6. The figure below represents two pulley wheels, centres A and B with a rubber band

CDEFGHC stretched round them. Radius of wheel centre A = 16cm, AB = 30cm. CD,

GF are tangents to the circles < CAB = 86.3°

a) calculate the length of the belt CD

b) Find the angle ABD

c) Find the length of the belt that would go round the pulleys (CDFGHC)

7. In the figure below, ABCD is a cyclic quadrilateral and BD is a diagonal. EADF is a straight line,

CDF = 68o, BDC = 45o and BAE = 98o.

Calculate the size of:

a) ABD.

b) CBD

8. A customer deposited Ksh.15,500 in a savings account. Find the accumulated amount

after 3½ years if interest was paid at 16% per annum compounded semi-annually

9. A retailer mixes three types of rice, Bismatti costing shs.120 per tin with Pishori costing shs.150

per tin and Ahero rice costing shs.80 per tin in the ratio x : 1 : 2 respectively. If he sells the

mixture at shs.137.50 per tin making a profit of 25%. Calculate the value of x.

10. Ashanti is a saleswoman and earns a commission on sales based on the monthly rates shown

in the table below:-

Sales (Kshs) | Commission rate % of sales |

The first 5000 | 10% |

The next 3000 | 15% |

Sales above 8000 | 20% |

In addition, she earns a basic monthly pay of Kshs.6700. During a certain month, she earned

a total salary amounting to Kshs.8368. How much worth of sales did she make?

11. The table below shows the annual income tax rates for a certain year.

Total income per month in Kshs. | Rates in Kshs. Per £ |

1-10164 10165 – 19740 19741 – 29316 29317 – 33892 388983 and above | 2 3 4 5 6 |

Automatic personal relief shs.1162 | |

Kiptoo earns a monthly salary of Kshs.25000. He is entitled to house and medical allowances

of Kshs.12000 and Kshs.3000 respectively

Calculate:

(a) His taxable income per month

(b) His monthly tax payable

(c)His annual tax payable

12. A company employee earns a basic salary of Kshs.25,000 and is also given taxable allowances

amounting to Kshs.10,480.

Monthly taxable income | Rate in Kshs. /Pound |

1- 4350 4351 – 8900 8901 – 13455 13451 – 18005 18006 and above | 2 3 4 5 6 |

Using the table of taxation above:-

(a) Calculate the employee’s taxable income

(b) If the employee is entitled to a personal tax relief of Kshs.800 per month, determine the net tax

(c) If the employee was given 40% increase in his income, calculate the percentage increase

in his income tax

13. A certain amount of money was invested at compound interest of 10% compounded

every two years for ten years. Given that the investor invested a total of 500,000/= at the

end of the ten years, find the amount of money invested to the nearest shillings

14. The cash price of a T.V set is Ksh. 26,000. Linda bought the set on hire purchase terms by

paying a deposit of Ksh. 6,000 and the balance by 24 equal monthly installments of

Khs. 1,045.30. Find the compound rate of interest per year.

.

15. What would Kshs.15000 amount to after 3years at 16% per annum compounded quarterly?

16 . Income rates for income earned were charged as follows:

Income in Kshs. p.m Rate in Kshs. per sh.20

1- 8400 2

8401- 18,000 3

18,001- 30,000 4

30,000 – 36,000 5

36,001 – 48,000 6

48,001 and above 7

A civil servant earns a monthly salary of Ksh.19,200. His house allowance is Ksh12,000 per

month. Other allowces per month are transport Ksh.1300 and medical allowance Ksh.2300.

He is entitled to a family relief of Kshs. 1240 per month.

Determine:

a) (i) His taxable income per month.

(ii) Net tax. b) In addition, the following deductions were made

NHIF shs. 230

Service charge Kshs. 100

Loan repayment Kshs. 4000

Co-operative shares of Kshs. 1200.

Calculate his net salary per month.

17. Use the taxation rates in the table below to answer the questions that follow;-

Taxable income in K £ p.a | Rate % per K£ |

1-4500 4501-7500 7501 – 10500 10501 – 13500 13501 – 16500 0ver 16500 | 10 15 20 25 30 35 |

The manager of a certain company is entitled to a monthly personal relief of shs.3000

and her tax (PAYE) is kshs.9000 per month she is also deducted NHIF shs.350 per month,

WCPS shs.800 per month and cooperative shares shs.1200 per month, calculate

(a) The managers total deductions per month

(b) Total tax per month

(c) The manager’s annual gross salary

(d) The manager’s monthly basic salary if her monthly allowance and medical allowances

are 10000 and 2000 shillings

18. The table below shows the income tax for a certain year;

Monthly taxable income (Kshs.) | Tax rates (%) |

1- 9680 9681- 18800 18801 – 27920 27921 – 37040 37940 and above | 10% 15% 20% 25% 30% |

In that year, Odero paid a net tax of Kshs.5,512 per month. His total monthly taxable allowances

amounted to Kshs.15,220 and he was entitled to a monthly personal relief of kshs.1,162.

Every month the following deductions were made;

N.H.I.F Kshs.320

Union dues Kshs.200

Co-operative shares Kshs.7,500

(a) Calculate Odero’s monthly basic salary in Kshs

(b) Calculate his monthly salary

19. (a) A car is worth shs.800,000 when new. During the first year it depreciates by 20%

of its value and in the second it deprecates by 5% of its value at the start of the year.

During the third, fourth and fifth year, depreciation rate is 10%. How much less will

it cost at the end of the fifth year?

(b) Find by how much the compound interest will exceed simple interest on shs.3,000

for two years at 15% per year

20. The table below shows the income tax rates:

Income per month (K£) Rate in Kshs per £

1 – 325 2

326 – 975 3

976 – 1300 5

1301 – 1625 6

Over 1625 7.50

Mr. Misoi is a public servant who lives in a government house and pays a nominal rent of Kshs.1,220 per month. He earns a basic salary of Kshs. 24,800 and a house allowance of Kshs.12,000 per month. He is entitled to a monthly relief of kshs.1620.

(a) Calculate his monthly;

(i) Taxable income in K£

(ii) Tax payable without relief

(iii) Tax after relief

(b) Apart from the income tax. The following monthly deductions are made from his earnings

-HELB loan repayment Kshs.2400

– Health insurance fund Kshs.1200

– 2% of Basic salary union fee

Calculate:- (i) the total monthly deduction made on Mr. Misoi’s income

(ii) Mr. Misoi’s net income per month

21. Joseph bought a camera on hire purchase (H.P) term by paying a deposit of shs.7200

and cleared the balance in 24 equal monthly installments each of 1250.

(a) find the hire purchase price of the camera

(b) the hire purchase price of the camera is 24% higher than the cash price. Find the

cash price of the camera

(c) Kangara took a loan from a financial institution and bought the camera with cash.

He repaid the loan at 18% p.a compound interest at the end of the two years. Find

the total interest paid by Kangara.

22. Income tax for all the income earned was charged at the rates shown.

Total Income p.a (K.£) | Rate in sh per K£ |

1 – 1980 1981 – 3960 3961 – 6440 6441 – 7920 7921 – 9900 Excess of 9900 | 2 3 5 7 9 10 |

(a) Wanyonyi earned a salary of Kshs.10,500 per month. In addition he was given a house

allowance of Kshs. 6500 per month. He got tax relief of Kshs. 300 per month.

Find (i) His taxable income p.a (ii) Income tax he pays per month. (b) A part from income tax the following deductions are made per month. NHIF of Kshs.320,

widow and pension scheme of 2% of his gross salary. Calculate his net monthly pay.

Commercial Arithmetic 2 Answers

1 | a) b) Total annually Monthly Less relief 1100.00 Net tax payable c) Total deductions Monthly income | M1 M1 A1 M1 M1 M1 M1 A1 B1 B1 | 1st and 2nd slabs 3rd and 4th slabs last slab Subtraction of relief Total deductions |

1. After 1st year = 95 x 4200000)

100

= Shs.357,000

After 2nd year = ( 87 x 357000)

100

= sh310590

After 3rd year = (88 x 310590

100

= shs.273319.20

After 4th year = ( 91 x 273319.20)

100

=shs.248720.50

After 5th year = (248720.50 x 93)

100 = shs.231310

The next 6years

A = 231310 (1- 0.05)6 = 170034.10

Then 140000 = 170034.10 (1-0.04)n

(0.96)n = 140000 = 0.8234

170034.10

n = log 0.8234

log 0.96

= 0.0844 = 4.76yrs

0.01773

Total no. of years = 5 + 6 + 4.76yrs = 15.76years

2. Gross tax = 4830 + 1120 + 600 = sh 6550 per month

Annual gross tax = 6550 X 12= 78,600

10 X 120,000 = sh.12,000

100

15 X 120,000 = sh.18,000

100

25 X 120,000 = sh. 30,000

100

Re. tax = 78600 – (12000 + 18000+30000)

=78600 – 60,000 = 18,6000

35 X x =18,600

100

0.35x = 18,600

x = sh 53142.86

Taxable income p.a = 36,000+53142.86

=sh.412142.86

Monthly salary = 413142.86 + 12,000

12

= 34428.57 + 1200 = Sh 35628.57

3. a) Sin 86.3° = XB/AB

Sin 86.3°= XB/30

XB = 30sin86.3°

XB = CD = 29.93746855 cm

b) < ABX = 90° - 86.3°

= 3.7°

< ABD = 3.7° + 90°

= 93.7°

c) < DBF obtuse = 360° - 187.4°

= 172.6°

Arc DEF = ø/360

D or ø/360 x2r

But cos 86.3° = AX/AB

Cos 86.3° = AX/30

AX = 1.935969248 cm

DB = 16 – 1.935969248 = 14.06403075 cm

Arc DEF = 172.6°/360° x 22/7 x 14.06403075

= 106807.8751

2520

= 42.38407742 cm

Arc CGH

< reflex CAG = 360° - (2x 86.3°)

= 187.4°

Arc CGH = 187.4°/360° x2 x 22/7 x 16

= 131,929.6

2520

= 52.35301587 cm

Total length of belt to go round the belt

= CD + DEF + GF + CHG

= 29.93746855 + 42.38407742 + 29.93746855 + 52.35301587

= 154.6120304 cm

4. ∠ABD = 310

∠ CBD = 370

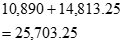

5. A = 15,000(1 + 8/100)7

= Ksh.25,707

6. Principle = 30,000 – 6,000

= 24,000/=

Amount = 18 x 2000

= 36,000/=

A = P 1 + r

A = P 1 + r

100

6,000 = 24000 1 + r

100

36000 = 1 + r

24000 100

3 = 1 + r

2 00

1 + r = 18 1.8

100

1 + r = 1.023

100

r = 0.023

100

⇒2.3%

7. Commission earned Kshs. (8368 – 6700) = Kshs. 1668/=

let sales in 3rd bracket be y

10/100 x 5000) + (15/100 x 3000) + (20/100 x y) = 1668

500 + 450 + 0.2y = 1668

0.2y = 1668 – 950 = 718

y = 718/0.2 = 35%

Total sales = (8000 + 3590)

= shs.11590

8. Find the principal which in 12 years at 5% p.a compound interest amounts to sh.450,00

. A = P (1 + R)n

100

I = A – P

A = (100 + R)n

100

I = P (100 + R)n – P

100

= P ( 100 + R/100)n – 1

450000 = P = 450000= 565397

9. a)Taxable income = (25000 + 12000 + 3000)= 40000

b) Income tax

10164 x 2/20 = Shs.1016.40

10164 x 3/20 = Shs.1524.60

10164 x 4/20 = Shs.2032.80

Remaining :

9508 x 5/20 = Shs.2377

Total tax payable p.m = 6950.8 – 1162 = Shs.5788.80

c) Annual tax payable = 5788.80 x 12 = Shs.69465.60

10. (a) taxable income = Kshs. 25000 + Kshs.10480

= Kshs. 35480

b) tax charged:

1st 4350 = 4350 x 2/20 = 683.25

2nd 4555 = 4555 x 3/20 – 683.25

3rd 4555 = 4555 x 4/20 – 911

4th 4555 = 4555 x 5/20 – 1138.75

Rem. 17465 = 17645 x 6/20 – 5239

Total tax – 8407.5

800.00

7607.50

(c) 40/100 x 35480 – 14.192 = 49672

New income = 35480 + 14192 = 49672

Remainder = 49672 – 18015 = 31657

Tax charged = 31657 x 6/20 =12665.1

Total tax = 12665.1

% increase in income ax = 4257.6 x 100

7607.5 = 55.97%

11. A = P(HR/100)n

500000 = P( 1+ 20)5

100

500,000 = (120/100)5

500,000 = P

(1.2)5

P = Shs.200,938.786 shs. 200,939

12. Principal = 26, 000 – 6,000 = 20,000

Total H.P instalments = 1045.3 x 24 = 25087.20

= 25087.20

25087.20 = 20,000 1 + r

100

1.254 = 1 + r

100

1.120 = 1 + r

100

r = 0.12 or 12%

100

13. No. of periods =12

r = 4% per period

A = 1.0412 x 15000

= 24015.5

14. a) i) taxable income = 19200 + 12000 + 1300 + 2300 = 34800

b) Net tax

8400 x 2/20 = 840

9600 x 3/20 = 1440

12000 x 4/20 = 2400

4800 x 5/20 = 1200

5800

Net tax = 5800 – 1240

= 4560

c) Net salary = 34800 – (4560 + 5530)

= 24710

15. (a) 9000 + 350 + 800 + 1200 = 11350

(b) 9000 + 3000 = 12000

(c) Total taxes = 12000 x 12

= shs.144000p.a

Taxes

450 x 2 = shs.9000

3000 x 3 = shs.9000

3000 x 4 = shs.12000

3000 x 5 = shs.15000

3000 x 6 = shs.18000

Shs.63,000

144000 – 63000= shs.81000

7y = 81000y = 11571

Taxable income= 4500 + 3000 x 4 + 11571 = K 28071p.a

Gross salary = shs. 561420p.a

(d) Total allowances = 12000 x 12

= 144,000

= 144,000

Basic salary = 561420

14400

Shs.417,420

Monthly basic pay = shs. 34785

16. (a) Net tax 5512

Add relief 1162

Tax payable 6674

Tax on 9680 earned

9680 X 10/100 = 968

Tax on 9120 earned

9120 x 15/ 100 = Shs. 1368

Tax on next 9120 x 20/100 = Shs.1824

Tax on next 9120 x 25/ 100 = 2280

Total 968 + 1368 + 1824 + 2280 = 6440

6674 – 6440 = 234

Let x be charged at 30%

30/100 X x = 234

X = 234 X 100 = Shs.780

30

Total chargeable Income

780 + (9120 x 3) + 9680 = 37820

Salary 37820 – 15220 = Shs.2260 per month.

b) Net salary (37820 – 1270 – 6674) = Shs.29876

17. a) 1st year after dep. Of 20%

800 000 x 80

100

= Khs. 640,000……………………………………………………

2nd year after dep. of 5%

= 640000 x 95

100

= 608,000 ……………………………….

The next 3 yrs

The next 3 yrs

A = P 1 – R = 608,000 ( 1 – 10) 3

100 100

= 698 000 (0.9)

= Sh. 443,232 ……………………………………………………

800,000 – 443,232 = Sh. 356,768 ……………………………………………………..

(b) S.I = 3000 x 15/100 x 2

= Sh 900 …………………………………………………

A = 3000 1 + 15

100

= 3000 1.15

= sh. 3967.50 ……………………………………………….

C.I = sh 967.50

967.50 – 900 = sh 67.50 ……………………………………….

18. (i) Taxable Income

115 x 24 800 + 12000 – 1220

100

= 28520 + 12000 – 1220

= Ksh.39,300

= K₤ 1965 p.m.

(ii) Tax due 325 x 2 = sh 650

650 x 3 = sh 1950

325 x 5 = sh 1725 ………………………..

325 x 6 = sh 1950

340 x 7.50 = sh 2250

Total tax = sh. 8825 P.m………………………

without relief

(b) (i) Total deduction

= sh (7280 + 2400 + 1200 + 2 of 24 800)……………….

100

= (7280 + 2400 + 1200 + 496) + 1220

= sh (11376 +_ 1220) = sh. 12,596 P.m …………………………………………

(ii) Net income = sh (24800 + 1200 – 12596) = sh. 24,204 P.m……………………………

19. a) Total instalments = (24 x 1250)= Shs.30000

H.P = 7200 + 30000= 37200

b) 124% = 37200

100% =

C.P = 100 x 37200

124

= 30000

c) A = 30000 (1 + 18/100)2

= 30000 (1.18)2 = 41772

Total interest = 41772 – 30000 = 11772

20. (a) (i) (10, 500 + 6,500) x 12 = K₤ 10,20 p.a

20

(ii) 1st 1980 x 2 = Kshs. 3960

2nd 1980 x 3 = Kshs 5940

3rd 2480 x 5 = Kshs. 12 400

4th 1480 x 7 = Kshs. 10360

5th 1980 x 9 = Kshs.17 820

Last 300 x 10 = Kshs 3 000

Kshs. 53 480

PAYE = 53480 – 300 x 12

12

= Shs. 4156.70

(b) Net monthly pay

17000 – 320 + 2 x 17000

100

= 17000 – 660

= Kshs 16 340.00