WAREHOUSING

This is an aid to trade involving the storing of goods and raw materials against atmospheric conditions, pests, theft, etc. Therefore, it is protection offered to goods when they are not required until they are needed.

WHY IS WAREHOUSING NECESSARY (FUNCTIONS OF WAREHOUSING)

- It enables a stock of goods to be stored until they are required.

- It enables manufacturers to continue with the production process as there is room to store the produced goods.

- Seasonal goods are kept for consumption during periods of no consumption.

- It facilitates preparation of goods for sale through advertising, sorting, weighing, packing, and branding of goods.

- It enables the storage of goods to prevent price fluctuations, especially with agricultural goods or products.

- It enables the importer or trader to look for the market while the goods are kept at the warehouse.

- It enables the breaking of bulk to meet the needs of individual retailers.

- It keeps the stored goods in strict and suitable conditions against bad weather and any form of contamination.

- It enables goods to be stored to meet a continuous flow of goods, thus avoiding scarcity.

TYPES OF WAREHOUSES

(a) Public warehouses.

These are privately owned by people whose business is to rent out spaces to those who may need temporary storage of stock. They are usually located at seaports, railway stations, and airports for any importer or exporter who has limited space in their premises. They are often used for storing goods for short periods while in transit.

(b) Private warehouses.

These are warehouses owned by private individuals for storing their goods. They may be for wholesalers or manufacturers who store their goods before sale.

(c) Bonded warehouses.

These are special warehouses where imported goods are kept until payment of customs duties is made. Goods are only released from the bonded warehouse after the customs duty is paid and a release warrant is issued.

(d) Free warehouses.

These warehouses keep goods that are not subjected to any customs duty or controlled by customs authorities.

ADVANTAGES OF BONDED WAREHOUSES TO THE IMPORTERS

- The importer may not pay the customs duty if the goods are bought while in bond, but it is passed on to the buyer.

- Goods may be advertised, blended, branded, and classified in the bonded warehouses.

- The importer may look for buyers before paying the customs duty.

- If the importer desires to re-export the goods, the customs duty is not paid but only storage charges.

- Some goods lose weight while in the bonded warehouse, so the customs duty paid becomes lower if it is based on the weight of goods (specific tax).

ADVANTAGES TO THE GOVERNMENT

- Bonded warehouses ensure that no duty is avoided (dodged) since the goods cannot be released without payment.

- They enable the government to check on prohibited goods and smuggling.

QUALITIES OR ESSENTIALS OF A GOOD WAREHOUSE

- It must be located in places where goods are produced in greater quantities and are used at mature stage.

- It should be fully equipped and have all the necessary facilities to store goods for a long time without being spoiled or damaged.

- It should be large enough to allow future expansion and storage of different types of goods safely.

- It should have a good transport system so that the goods do not go bad due to delayed delivery to the market. It would also facilitate the transportation of raw materials to production centres.

- It should have efficient staff to acquire efficiency and protect goods against any loss or damage.

- It should have adequate protection measures so that chances of losses or damages are prevented by all means possible.

- It should be located as near as possible to the buyers so that the transport cost to the market is minimized.

- It should stock goods according to people’s demand to avoid wastage of goods and money (resources).

ORGANIZATION OF WAREHOUSES / MANAGEMENT OF WAREHOUSE

In the organization of a warehouse, the owner is on top of the list followed by the general manager who is usually the chief executive. A warehouse has the following departments with their responsibilities:

(a) PURCHASES DEPARTMENT.

This department is headed by a purchasing manager responsible for buying stock for the warehouse. Its major duties are:

- Placing orders for goods needed in the warehouses with the most suitable manufacturer.

- Looking for cheap sources of supply so that a businessman can make high profits.

- Assessing changes in fashion and tastes so that only goods demanded are stored in a warehouse, avoiding losses to the businessman.

- Receiving goods from the suppliers and making sure that they are safely stored.

- Maintaining a list of regular suppliers for easy contact and purchasing of goods when required.

- Responsible for packing, blending, or branding goods, ensuring that goods are ready for sale.

- Maintaining store records to show receipts issued and balance in stock.

(b) SALES DEPARTMENT

This is headed by a sales manager who is responsible for the profitability of the entire business. It is responsible for the following:

- Carrying out sales promotion strategies such as advertising, branding, free samples, etc.

- Receiving orders from customers and dispatching goods as required by the buyer.

- Maintaining the list of all regular customers, classifying them according to areas or creditworthiness to attend to them appropriately.

- Arranging for the transport of goods from the warehouse to the retailer’s premises according to the agreed terms.

- Handling customer complaints regarding the goods supplied and ensuring appropriate steps are taken to solve related problems.

- Ensuring that required goods are available to avoid strategies that may cause price fluctuations.

- Maintaining a regular sales force and arranging for its traveling to acquire efficiency in the warehouse.

- Ensuring credit control to avoid incurring bad debt.

(c) ACCOUNTS DEPARTMENT.

This is headed by a chief accountant and handles all accounting work. The major activities include:

- Receiving and effecting payments on behalf of customers.

- Preparing budgets and enforcing costing systems to ensure proper accountability of warehouse funds.

- Ensuring that all financial commitments of the business are conveniently met.

- Carrying out financial accounts at the end of each year in the form of preparing the balance sheet.

- Preparing invoices and statements to be sent to customers for accountability.

- Preparation of wage sheets and payment of wages.

(d) SECRETARY DEPARTMENT

It is headed by the secretary or office manager and handles all correspondence, legal affairs, personnel matters, and records. Responsibilities include:

- Keeping up to date with correspondence, which may be regarding sales of goods.

- Maintaining necessary files to ensure smooth running of the business.

- Advising management on matters of legal importance, e.g., company registration, dividends.

- Appointing staff members or advising the general manager and owner on senior employee appointments.

- Arranging training of personnel to ensure efficiency in duties performed by staff.

- Maintaining staff records for reference in promotions and other appointments.

(e) SALES PROMOTION DEPARTMENT.

It is headed by the sales promotion manager who is responsible for:

- Handling all advertisements aimed at promoting sales.

- Printing catalogs, prices, and other documents to be sent to prospective buyers.

- Arranging special demonstrations of goods offered by the business to promote sales volume.

- Participating in trade shows like SABA-SABA trade fair and international trade fairs to interact with prospective buyers.

- Attending to customer complaints and ensuring such complaints are resolved.

STOCK ADMINISTRATION

Stock administration is the management of stocks in a business so that goods for sale are always in sufficient quantities without running short of supplies or carrying more stock than the recovered turnover.

FUNCTIONS/ACTIVITIES IN STOCK ADMINISTRATION

The main activities or functions of stock administration are:

- STOCK CONTROL

Keeping and checking records of stock in the firm. Stock control is the main activity in stock administration. - ISSUING OF STOCK

Releasing sold stock to customers. - RECEIVING STOCK

Taking delivery of goods from suppliers. - CARE OF STOCK

Keeping stock in good order and at the right place. - STOCK TAKING

The process of finding the quantity of stock held at a specific period. This includes:- Checking pilferage.

- Checking accuracy of records.

- Checking weaknesses in the system of stock control.

- Supporting the value of closing stock used for final accounts.

- PLACING OF ITEMS

Allocating goods in appropriate places. Stock must be arranged to reveal old items from new ones. - STOCK VALUATION

Finding the value of stock held at a specific period, e.g., value of stock at the end of the year.

STOCK LEVELS

There are various points of stock volume at different times. Stock levels include:

- Minimum stock

- Maximum stock

- Average stock

- Order point / Re-order point

MINIMUM STOCK

This is the lowest amount which should be kept to safeguard against unforeseen events like delays in deliveries.

It is the quantity of a certain commodity that should always be in stock to safeguard sales against unforeseen delays.

It is the level below which the stock of any given commodity should not fall.

Minimum stock = order point – (Normal consumption × lead time).

MAXIMUM STOCK

This is the highest level of stock recorded after receipt of new deliveries. It is the level reached immediately upon receipt of new supply of goods.

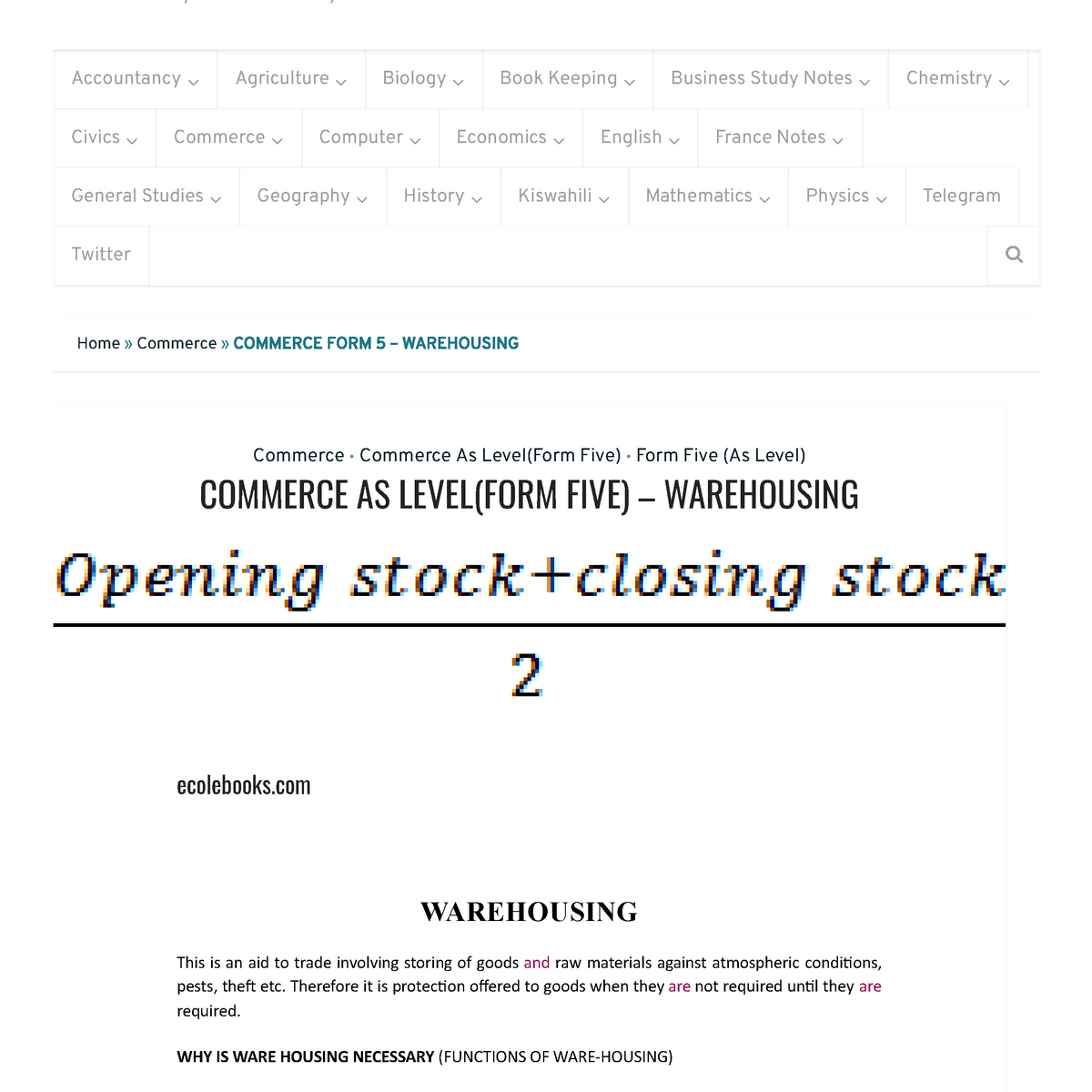

AVERAGE STOCK

This refers to the average stock level within a period, usually a year. Average stock can be calculated as follows:

Average stock = ![]()

ORDER POINT

This is the level at which placing a new order must be done.

It is the level at which a new order is required.

Determinants of stock order are:

- Daily sales / wages / consumption

- The period between placing order and receiving delivery / minimum stock level.

Order point = (Daily sales × time of delivery) + minimum stock

Example 1

From the data given, calculate order point:

- Daily sales: 100 kg

- Delivery time: 3 days

- Minimum stock: 200 kg

Solution:

Order point = (100 × 3) + 200 = 300 + 200 = 500 kg

Example 2

Given the following data of sales:

- Daily volume of sales = 50 tonnes

- Time of delivery = 12 days

- Minimum stock = 200 tonnes

Calculate order point.

Solution:

Order point = (50 × 12) + 200 = 600 + 200 = 800 tonnes

ECONOMIC ORDER QUANTITY (EOQ)

This is the amount of quantities delivered from the supplier of materials. Economic order quantity is given by the formula below:

![]()

Where:

- C = ordering cost per order

- D = demand per annum

- Cc = carrying cost per item per annum

Example

Find the economic order quantity where demand is 20,000 units per annum, the ordering cost is Tshs. 500 per order, and the carrying cost per item per annum is Tshs. 120.

Solution:

![]()

Demand per annum = 20,000 units

Carrying cost per item = Tshs. 120

Ordering cost = Tshs. 500

![]()

![]()

![]()

STOCK TAKING

This is the process of verifying the balances of items held in stock at the end of a predetermined period by counting, weighing, and measuring. Stock taking can be divided into three categories:

- ANNUAL STOCK TAKING

Done once per year to find the ending balance for preparing financial reports. - PERIODIC STOCK TAKING

Finding the balances of stock for an interval period. - PERPETUAL STOCK TAKING

Continuous stock taking by recording transactions of receiving and issuing materials in stock.

CALCULATING CONTROL LEVELS

- LEAD TIME

The period between ordering and replacement, i.e., when goods are available for use. - RE-ORDER LEVEL

The stock level at which a further replacement order should be placed.

Re-order level = maximum usage × maximum lead time.

Minimum level = Re-order level – (Normal consumption × lead time).

TURNOVER

Turnover refers to total sales during a certain period.

Turnover = price × quantity = P × Q

RATE OF STOCK TURNOVER

This is the number of times the average volume of stock held has been turned over, i.e., sold during a given period.

Rate of stock turnover = ![]()

GROSS PROFIT

This is the excess of sales (turnover) over the cost of sales.

G.P = Total sales – Cost of sales.

Example 1

Given:

- Sales = 120,000

- Purchases = 100,000

Gross profit = 120,000 – 100,000 = 20,000

Example 2

Given the following data of a firm:

- Opening stock at the beginning of the year = 250,000

- Purchases = 300,000

- Closing stock at the end of the year = 20,000

- Goods returned to supplier (Returns outwards) = 10,000

- Goods returned by customers (Returns inwards) = 20,000

- Total sales = 800,000

Find gross profit.

Opening stock 250,000 Add: Purchases 300,000 Less: Returns outwards 10,000 Net purchases 290,000 Goods available for sale 540,000 Less: Closing stock 20,000 Cost of goods sold 520,000 Gross profit 260,000 780,000 | Sales 800,000 Less: Returns inwards 20,000 Net sales 780,000 |

NET PROFIT

This is the revenue remaining after deducting expenses of running a business.

To calculate net profit, a profit and loss account must be drawn up, showing on the credit side the gross profit brought forward from the trading account and on the debit side, various expenses such as rent, rates, taxes, wages, insurance, interest on loans (if any), advertising, light and heat, depreciation, etc.

Net profit = gross profit – expenses

BUSINESS CALCULATIONS

(a) MARK-UP

This is gross profit as a percentage of cost price.

Mark-up = ![]() × 100

× 100

Example

Given:

- Cost price = 50,000

- Gross profit = 25,000

Mark-up = ![]() = 50%

= 50%

(b) MARGIN

This is the gross profit as a percentage of sales price.

Margin = ![]() × 100

× 100

Example

Given:

- Selling price = 100,000

- Gross profit = 20,000

Margin = ![]() = 20%

= 20%

DISCOUNTS

This is the allowance given to the trade on goods purchased. There are three types of discounts.

(a) TRADE DISCOUNT

This is an allowance (deduction) made if goods are sold by one businessman to another on goods whose price is either fixed, controlled, or generally known.

Example:

Mr. Bukagile sells his products at Tshs. 1000 per unit. He gives a trade discount of 10%. If a customer bought 50 units, the trade discount will be:

(50 × 1000) × 10% = 5,000

(b) QUANTITY DISCOUNT

This is the discount allowed in addition to a trade discount if the quantity of goods sold is large.

Example:

A wholesaler selling soda may allow a trade discount to retailers of 20% for quantities less than 50 crates and an additional quantity discount of 5% for any amount exceeding 50 crates.

(c) CASH DISCOUNT

This is a discount given to induce the trader to pay promptly.

Example: 5% discount will be allowed if payment is made within 1 month, 2% if payment is made after 1 month, and 1% if payment is made after more than a month.

TYPES OF CASH DISCOUNT

- (i) DISCOUNT ALLOWED

This is the amount allowed to the debtor. It is an expense to a business. - (ii) DISCOUNT RECEIVED

This is a discount received from creditors.

DOCUMENTS USED IN WAREHOUSING

- Warehouse warrant.

This is a document authorizing the removal of goods. It is issued to the importer after storing goods in a warehouse. - In-bond notes.

This document shows the amount of goods held in a warehouse.

2 Comments