THE PETTY CASH BOOK

Definition

The petty cash book is the cash book used to record small expenses or expenditures which take place from time to time within the business.

OR

It is the book used to record the small expenditure incurred by the business or organization for a certain period of time such as day to day, week to week, or month.

PETTY CASHIER

A petty cashier is a person who receives money in order to meet petty expenditures.

ADVANTAGES OF PETTY CASH BOOK

- It helps the main cashier to deal with small payments.

- It facilitates small payments without the use of cheques.

- It is easy to check the petty cashier because the amounts are small.

THE PETTY CASH VOUCHER / PAYMENT VOUCHER

These vouchers are filled by the petty cashier when payments are made. These vouchers prove that payment has been made.

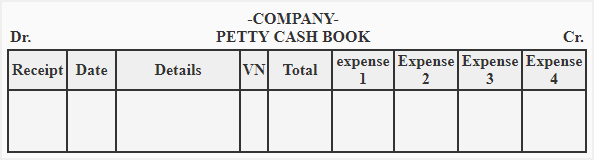

STRUCTURE OF PETTY CASH BOOK

The petty cash book has two sides: the received side and the payment side.

THE TYPES OF EXPENSES MADE THROUGH PETTY CASH

- POSTAGE including parcel, telegram, stamp.

- STATIONERY including small items such as ink, books, printing.

- TRAVELING EXPENSES including petrol, tires, etc.

- SUNDRY ITEMS such as sugar, milk for office tea.

THE STRUCTURE OF PETTY CASH BOOK | |||||||||||

| AMOUNT RECEIVED | FOLIO | DATE | DETAIL | PAYMENTS | ANALYSIS OF PAYMENTS | ||||||

| V.No | Total | Postage | Stationery | Traveling exp. | G. Expenses | ||||||

EXAMPLE:

On 1st March, Hamisi received from chief cashier Tshs 40,000/=.

March 2: Paid for telegram 2,000/=.

March 3: Paid for postage 6,000/=.

March 4: Paid for bus fare 2,000/=.

March 5: Paid for office cleanliness 3,200/=.

March 6: Stationery 8,000/=.

Required: Draw up a petty cash book.

EXERCISE 1:

Enter the following transactions in the petty cash book of F. Funds with columns for (i) postage and telegram, (ii) stationery, (iii) traveling, (iv) office expenses in the year 2010.

Jan 1: Receive petty cash 100,000/=.

Jan 1: Paid for sugar 7,000/=.

Jan 2: Bought stamps 20,000/=.

Jan 3: Paid for pencil 5,000/=.

Jan 5: Bus fare 2,000/=.

Jan 8: Telegram 15,000/=.

Jan 9: Envelopes 4,000/=.

Jan 11: Coffee 9,000/=.

Jan 15: Cleaning 2,000/=.

EXERCISE 2:

Enter the following transactions of Machanga Cooperative Society in the petty cash book under the columns for postage, water charge, transport charge, electricity, stationery.

On Jan 1, 2009, the petty cashier received Tsh 100,000 petty cash.

Jan 2: Paid water charge – 10,000/=.

Jan 3: Paid electricity charge – 6,000/=.

Jan 4: Bought stationery – 30,000/=.

Jan 10: Paid transport charge – 10,000/=.

Jan 13: Bought stamps – 20,000/=.

Jan 15: Bought stationery – 5,000/=.

Jan 18: Paid transport charge – 10,000/=.

Jan 27: Paid water charge – 30,000/=.

Jan 29: Paid electricity expenses – 20,000/=.

Jan 30: Transport charge – 20,000/=.

Jan 31: Bought stamps – 20,000/=.

THE IMPREST SYSTEM

The imprest system is where a refund is made of the total paid out in the period.

It is when a cashier gives the petty cashier enough cash to meet his needs for the following period. At the end of the period, the cashier finds out the amount spent by the petty cashier and gives him an amount equal to what was spent. The petty cash in hand should be equal to the original amount with which the period was started. This system is known as the IMPREST SYSTEM and the amount is called CASH FLOAT.

Example 1

The cashier gives petty cashier 50,000.

The petty cashier paid out during a week 34,570.

The balance of the petty cash at the end of the week is 5,430.

The cashier now gives the petty cashier 34,570.

The petty cashier hands over at the end of the period 50,000.

Example 2

The petty cashier of ABC Secondary has a cash float of Tshs 200,000/=. If Tshs 146,000 and 4,000 was spent on purchases of stationery and entertainment of teachers respectively, how much will be reimbursed by the chief accountant to petty cashier?

Cash float given by chief cashier: 200,000

Less expenses made by petty cashier:

Purchases (stationery): 146,000

Entertainment to teachers: 4,000

Total amount spent: 150,000

CASH BALANCE: 50,000

Therefore, 150,000 will be reimbursed to petty cashier to restore the imprest system of cash float 200,000 given.

EXAMPLE 3:

Enter the following transactions in petty cash book showing analysis columns for carriage, traveling expenses, and stationery. Restore the imprest and bring down the balance for the commencement of the following month.

Feb 1: Petty cashier in hand Tshs 25,000.

Feb 2: Paid bus fare Tshs 3,700, carriage Tshs 1,400.

Feb 3: Paid bus fare Tshs 1,800, office expenses Tshs 1,200.

Feb 3: Bought stationery for Tshs 4,700.

Feb 4: Paid carriage Tshs 1,900, bus fare Tshs 2,500.

Feb 5: Bought stationery for Tshs 2,300.

Feb 6: Paid office expenses for Tshs 1,500.

Balance the book as of 8th Feb 2009.

EXAMPLE 4

Kassim employs a cashier who keeps a petty cash book on the imprest system. It has five analysis columns for postage, travelling, stationery, general expenses, and ledger account. Rule a petty cash book and record the following week’s transactions inserting appropriate folio numbers and petty cash voucher numbers.

2002 Jan 11th: Drawn imprest of 2,000/=, pays postage Tshs 145/=, bus fare Tshs 65/=, pays Mattew account Tshs 208/=.

2002 Jan 12th: Pays fares Tshs 26/=, pays for note papers Tshs 55/=, collects from staff for private telephone calls Tshs 298/=.

2002 Jan 13th: Pays for cleaning materials Tshs 28/=, pays for tea and calls for typist’s birthday Tshs 36/=.

2002 Jan 14th: Pays L. Sasa account Tshs 225, pays for cleaning materials Tshs 130/=.

2002 Jan 15th: Pays cleaner wages Tshs 500, pays fares Tshs 12, pays window cleaner Tshs 25/=.

Also rule off the book, bring down the balance in hand and restore the imprest to Tshs 2,000/= as on 15th January 2002.

EXERCISE 1

Rule a petty cash book with analysis columns for stationery, motor expenses, cleanliness, traveling, and ledger.

The float is Tshs 150,000/= for one week.

May 1: Received cash for the float.

May 2: Bought brooms Tshs 8,000/=, notebook Tshs 5,000/=, and paid bus fare Tshs 3,000/=.

May 3: Bought engine oil Tshs 15,000/=, typing papers Tshs 12,000/=, and paid bus fare Tshs 3,000/=.

May 4: Bought u-bolt for van Tshs 3,000/=.

May 5: Paid Fredy a supplier Tshs 18,000/=.

May 6: Paid motor mechanic Tshs 20,000/=, bought office paints Tshs 4,000/=.

May 7: Paid office cleaner Tshs 15,000/=.

Required:

- Record the transactions in the said petty cash book.

- Post to ledger account at May 7th.

EXERCISE 2

The following transactions relate to Hamisi for the month of October 2003.

Oct 1: The main cashier gave 150,000/= float to petty cashier. Payments during the month were as follows:

Oct 2: Purchased marking pen 9,000/=.

Oct 2: Purchased sugar for Headmaster 5,000/=.

Oct 3: Purchased petrol 2,000/=.

Oct 4: Paid Mr. Isiyo 5,000/=.

Oct 5: Postage 7,000/=.

Oct 5: Cleaning expenses 3,500/=.

Oct 6: Petrol 2,200/=.

Oct 7: Traveling expenses 6,000/=.

Oct 8: Paid Mama Patel 10,000/=.

Oct 9: Paid Mr. Dogo as entertainment 8,000/=.

Oct 10: Postage 2,500/=.

Oct 11: Sundry expenses 2,400/=.

Oct 12: Paid Mr. Chidio 5,000/=.

Oct 15: Petty cash was reimbursed as the bursar was traveling on duty.

Required: Prepare the petty cash book.

Use analysis columns as stationery, office expenses, petrol, traveling expenses, cleaning, entertainment, and ledger.