DEPARTMENT ACCOUNT

For an enterprise with about four or five branches, it is important to know the profit obtained in each branch or department.

This is obtained by opening a Trading, Profit, and Loss Account for each year ended.

An example of a department is a chain or departmental store.

Every department carries on business by buying and selling different commodities with the aim of making profit.

Example:

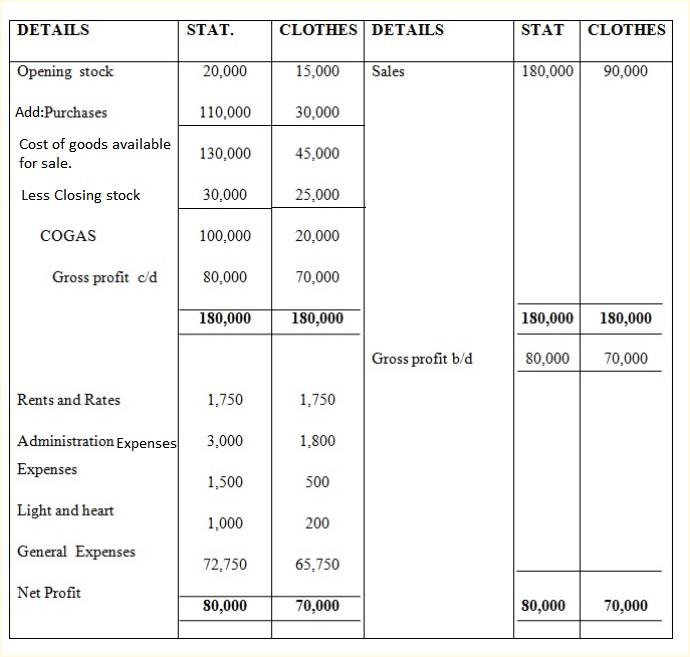

Ubungo Islamic School has two departments in their store: Stationery department and Clothes department.

| Description | Stationery | Clothes |

|---|---|---|

| Stock of goods Jan | 20,000 | 15,000 |

| Purchases | 110,000 | 30,000 |

| Stock of goods Dec | 30,000 | 25,000 |

| Salary | 180,000 | 90,000 |

Expenses were as follows:

- Rent and Rates: Stationery dept – 1,750; Clothes dept – 1,750

- Administration expenses: Stationery dept – 3,000; Clothes dept – 1,800

- Heat and lighting: Stationery dept – 1,500; Clothes dept – 500

- General expenses: Stationery dept – 1,000; Clothes dept – 200

Required:

Show Department Trading, Profit & Loss Account.

Solution:

DR. DEPARTMENTAL TRADING, PROFIT & LOSS A/C FOR THE YEAR ENDED CR

ALLOCATION OF EXPENSES OF DEPARTMENTS

Departmental expenses can be divided as follows:

- Equally: Includes expenses such as salary for a manager, general expenses, all expenses which benefit all departments, advertising.

- In the ratio of Sales (Turnover): Includes expenses such as advertisement, carriage outwards, commission on sales, discount allowed, bad debts, returns inward, etc.

- In the ratio of Purchases: Includes expenses such as carriage inwards, discount received, returns outwards, purchasing tax, warehousing, wages, etc.

- Floor space occupied (Area): Includes expenses like rent and rates, lights and heating, insurance for building, repairs, premises insurance, and all expenses related to maintenance of premises.

- In the ratio of number of employees: For example, staff salary, staff welfare, staff canteen expenses.

- Direct apportioned to Department: Includes depreciation on equipment used by one department and in no way benefits other departments.

Expenses to any department or incurred specifically for that department should be charged to that department.

Example:

Ahmed runs his business in three departments: Books, Stationery, and Clothes. The following information was extracted from his books:

- Capital: 250,000/=

- Purchases: Books 90,000/=, Stationery 120,000/=, Clothes 210,000/=

- Sales during the year: Books 150,000/=, Stationery 250,000/=, Clothes 350,000/=

- Stock Jan 2003: Books dept 10,890/=, Stationery dept 11,220/=, Clothes dept 25,000/=

- Stock Dec 31, 2003: Books dept 11,210/=, Stationery 13,100/=, Clothes dept 28,300/=

- Wages and salaries: 13,800/=

- Rent and Rates: 10,800/=

- Staff welfare: 8,400/=

- Light and heating: 7,500/=

- Advertising: 4,500/=

- Carriage inwards: 28,000/=

- Carriage outwards: 1,800/=

The following information about departments is available:

| Description | Books | Stationery | Clothes |

|---|---|---|---|

| Floor area occupied | 320 | 400 | 480 |

| Number of employees | 12 | 18 | 20 |

Required:

- Apportion expenses according to a suitable basis.

- Draw up Department Trading, Profit and Loss Account.

Working:

Expenses:

1) Wages and salaries (13,800) (No. of employees)

Ratio: 12 : 18 : 20 = 6 : 8 : 10 = 24

Books: 6/24 × 13,800 = 3,450

Stationery: 8/24 × 13,800 = 4,600

Clothes: 10/24 × 13,800 = 5,750

2) Rent and Rates (10,800) (Area occupied)

Ratio: 320 : 400 : 480 = 4 : 5 : 6 = 15

Books: 4/15 × 10,800 = 2,880

Stationery: 5/15 × 10,800 = 3,600

Clothes: 6/15 × 10,800 = 4,320

3) Staff welfare (8,400) (No. of employees)

Books: 6/24 × 8,400 = 2,100

Stationery: 8/24 × 8,400 = 2,800

Clothes: 10/24 × 8,400 = 3,500

4) Light and heating (7,500) (Area occupied)

Books: 4/15 × 7,500 = 2,000

Stationery: 5/15 × 7,500 = 2,500

Clothes: 6/15 × 7,500 = 3,000

5) Advertising (4,500) (Equally)

Books: 1/3 × 4,500 = 1,500

Stationery: 1/3 × 4,500 = 1,500

Clothes: 1/3 × 4,500 = 1,500

6) Carriage inwards (28,000) (Ratio of purchases)

Purchases: Books 90,000; Stationery 120,000; Clothes 210,000

Ratio: 3 : 4 : 7 = 14

Books: 3/14 × 28,000 = 6,000

Stationery: 4/14 × 28,000 = 8,000

Clothes: 7/14 × 28,000 = 14,000

Carriage outwards (1,800) (Ratio of sales)

Sales: Books 150,000; Stationery 250,000; Clothes 350,000

Ratio: 3 : 5 : 7 = 15

Books: 3/15 × 1,800 = 360

Stationery: 5/15 × 1,800 = 600

Clothes: 7/15 × 1,800 = 840

DR DEPARTMENTAL TRADING, PROFIT & LOSS A/C CR

DEPARTMENTAL BALANCE SHEET AS AT

ENTER DEPARTMENT TRANSFER

Purchases made for one department may be sold in another department. In such a case, the item should be deducted from the figure for purchases of the original purchasing department and added to the figure for purchases of the subsequent selling department.

EXERCISE

The following information was extracted from a trader who maintains a department store with Department A and B:

| Description | Dept A | Dept B |

|---|---|---|

| Purchases | 52,800 | 43,600 |

| Sales | 160,000 | 124,000 |

| Opening stock | 14,600 | 11,240 |

| Closing stock | 12,400 | 8,654 |

Other income:

- Discount Received: 1,446

- Commission Received: 2,880

Expenses:

- Delivery expenses: 1,800

- Insurance: 2,816

- Advertising: 1,296

Additional information:

- Advertising expenses to be apportioned equally.

- Delivery to be apportioned on sales.

- Insurance to be apportioned in the ratio 6:5 respectively.

- Other income to be apportioned as follows:

- Commission received should be proportionate to 1.5% of purchases. Tshs. 1,400 made by Department A was sold in Department B.

Show:

Department Trading, Profit and Loss Account in column form for the year ended 31 Dec. 2009. Show all your working.

Working:

- Advertising 1,296

Dept A: ½ × 1,296 = 648

Dept B: ½ × 1,296 = 648 - Delivery expenses 1,800

Sales = 160,000 + 124,000 = 284,000

Dept A: 160,000 / 284,000 × 1,800 = 1,014

Dept B: 124,000 / 284,000 × 1,800 = 786 - Insurance 2,816 (6:5 ratio)

Dept A: 6/11 × 2,816 = 1,536

Dept B: 5/11 × 2,816 = 1,280 - Commission received 2,880

Sales: A 160,000; B 124,000

Dept A: 20% × 160,000 = 32,000

Dept B: 20% × 124,000 = 24,800

Dept A: 320 / 568 × 2,880 = 1,623

Dept B: 248 / 568 × 2,880 = 1,257 - Discount received 1,446

Purchases: A 52,800; B 43,600

Dept A: 3/200 × 52,800 = 792

Dept B: 3/200 × 43,600 = 654

792 + 654 = 1,446

Dept A: Purchases 52,800

(-) Goods transfer – 1,400

= 51,400

Dept B: Purchases 43,600

(+) Goods transfer 1,400

= 45,000

DR. DEPARTMENTAL TRADING, PROFIT & LOSS A/C FOR YEAR ENDED CR

EXERCISE 1

Kelvin department store has three departments: Electrical, Furniture, and Leisure goods. From the details given below, you are required to draw up the trading account of the firm for the year ended 31st Dec 2001 for each department and in total.

01/01/2001 – 31/12/2001

- a) Stock

- Electrical: 72,960/= (Opening), 95,040/= (Closing)

- Furniture: 207,576/= (Opening), 193,800/= (Closing)

- Leisure: 172,440/= (Opening), 268,740/= (Closing)

- b) Sales of the year

- Electrical: 358,080/=

- Furniture: 876,720/=

- Leisure: 565,200/=

- c) Purchases of the year

- Electrical: 218,340/=

- Furniture: 655,584/=

- Leisure: 328,656/=

- d) Other expenses

- Transport: 120,000/=

- Other trading expenses: 45,000/=

- e) Other expenses are to be distributed to other departments on the basis of sales.

1 Comment